Over the last two years, many of my friends have gotten hitched. Maybe it’s because breaking the psychological barrier of 30 gives you new perspective. Maybe it’s because in this country there’s an unwritten rule that says you need to be married by at least 31 otherwise which questions will be raised. Recently I met a friend who mentioned how he wanted to make responsible choices like own a house and save for his unborn children. A far cry from the type of choices the fellow made between Pol and Gal only a few years ago.

Home ownership in the country is viewed differently by people of different economic and social backgrounds. A person living in suburban or rural Sri Lanka entitled to an ancestral home may be quite content with travelling to the city in public transport while living in the Mahagedara. Some others might inherit land on which they plan to build a home. Some may wish to build or buy property on their own as a mark of financial growth and independence. Without getting too tedious about this, my point is each person has different requirements depending on their financial prognosis and objectives.

While we can build various models based on each individual’s circumstances using different projections, I have focused on a few scenarios relevant to my friend over a 10 year period. He essentially wanted to find out if it was worthwhile building a house rather than renting it over a period.

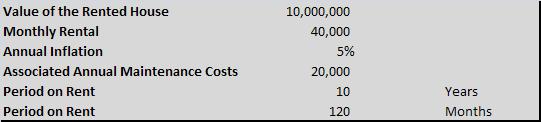

Renting a House for a 10 year period

Costs of relocation such as broker fees and lawyer charges are factored within the annual costs.

With 5% annual Inflation affecting rent and other costs, the total cost of renting over a 10 year period is 6.163 million. This is fairly straight forward and requires no explanation.

Buying/Building a House on a Loan

Suppose this guy thought renting was a waste of money and planned to buy/build a house worth 10 million on a loan.

Obviously paying 134,935 as a monthly loan rental on a house that you can rent for 40,000 might seem a little farfetched, but let’s see where this takes us. After 10 years it has cost him 16.192 million for a house he bought for 10 million.

What happens if he had the bright idea to save the money which can be paid towards a loan while still renting the house? For example the family can afford to pay 1.619 million on loans per year but choose to rent and save the extra money they earn.

In this scenario (after a lot of assumptions) they manage to save 15.077 million by not going for the loan.

Both scenarios have advantages and disadvantages. By not going for a loan they may have more independence to take on discretionary expenses and are better suited to meet emergencies. However after 10 years the asset is only 15 million of cash. While owning a home gives you security and peace of mind, there may be other expenses such as replacements, repairs and taxes.

Buying a second home – Lump sum payment

Moving on from my friend, what if you already own a home and pay no rent. You have disposable cash that you wish to invest in a house. One way to do this is with a lump sum payment.

You pay 10 million which idles around your house and buy a house, then rent it out under the following assumptions.

You reinvest the annual rent in an account which pays 8% per annum and end up with 8.31 million plus a house worth more than 10 million in 10 years.

What if you directly deposit the money at 8% per annum for 10 years?

Under this scenario if the house can be sold for above 13.2 million after 10 years, your gamble of buying a house as opposed to parking your money in a bank will be worthwhile.

Buying a second home – On a Loan

What if a loan was taken out and it was serviced with the rental income from the house.

If opportunity costs are taken into account it actually costs 15.619 million to finish paying the loan.

In summary I looked at five options.

If property prices increase according to given estimates the investment will yield you excess returns. Here’s an example of price increases over the last 10 years. The values are from classified advertisements from 2005 and 2015. While the valuations may not be for exactly comparable properties the trend is upwards.

The general suggestion of this post is that home ownership comes with financial benefits. However, if you are not comfortable with debt or can’t find or build your ideal home within your budget, invest the excess income for the future so you won’t be too far behind life’s possibilities.